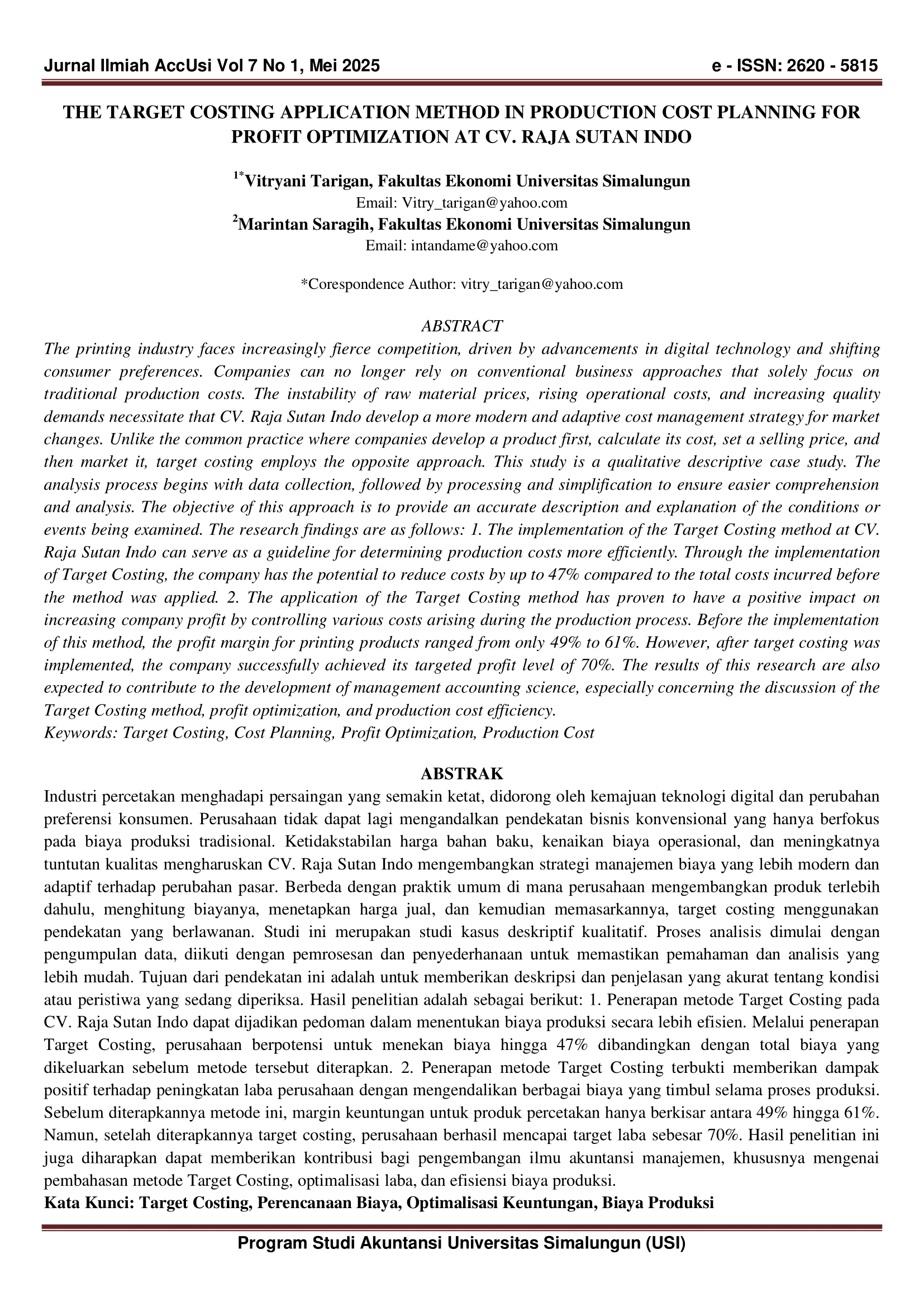

The Target Costing Application Method in Production Cost Planning for Profit Optimization At CV. Raja Sutan Indo

DOI:

https://doi.org/10.36985/rgtw7f82Keywords:

Target Costing, Cost Planning, Profit Optimization, Production CostAbstract

The printing industry faces increasingly fierce competition, driven by advancements in digital technology and shifting consumer preferences. Companies can no longer rely on conventional business approaches that solely focus on traditional production costs. The instability of raw material prices, rising operational costs, and increasing quality demands necessitate that CV. Raja Sutan Indo develop a more modern and adaptive cost management strategy for market changes. Unlike the common practice where companies develop a product first, calculate its cost, set a selling price, and then market it, target costing employs the opposite approach. This study is a qualitative descriptive case study. The analysis process begins with data collection, followed by processing and simplification to ensure easier comprehension and analysis. The objective of this approach is to provide an accurate description and explanation of the conditions or events being examined. The research findings are as follows: 1. The implementation of the Target Costing method at CV. Raja Sutan Indo can serve as a guideline for determining production costs more efficiently. Through the implementation of Target Costing, the company has the potential to reduce costs by up to 47% compared to the total costs incurred before the method was applied. 2. The application of the Target Costing method has proven to have a positive impact on increasing company profit by controlling various costs arising during the production process. Before the implementation of this method, the profit margin for printing products ranged from only 49% to 61%. However, after target costing was implemented, the company successfully achieved its targeted profit level of 70%. The results of this research are also expected to contribute to the development of management accounting science, especially concerning the discussion of the Target Costing method, profit optimization, and production cost efficiency

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Vitryani Tarigan, Marintan Saragih (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.