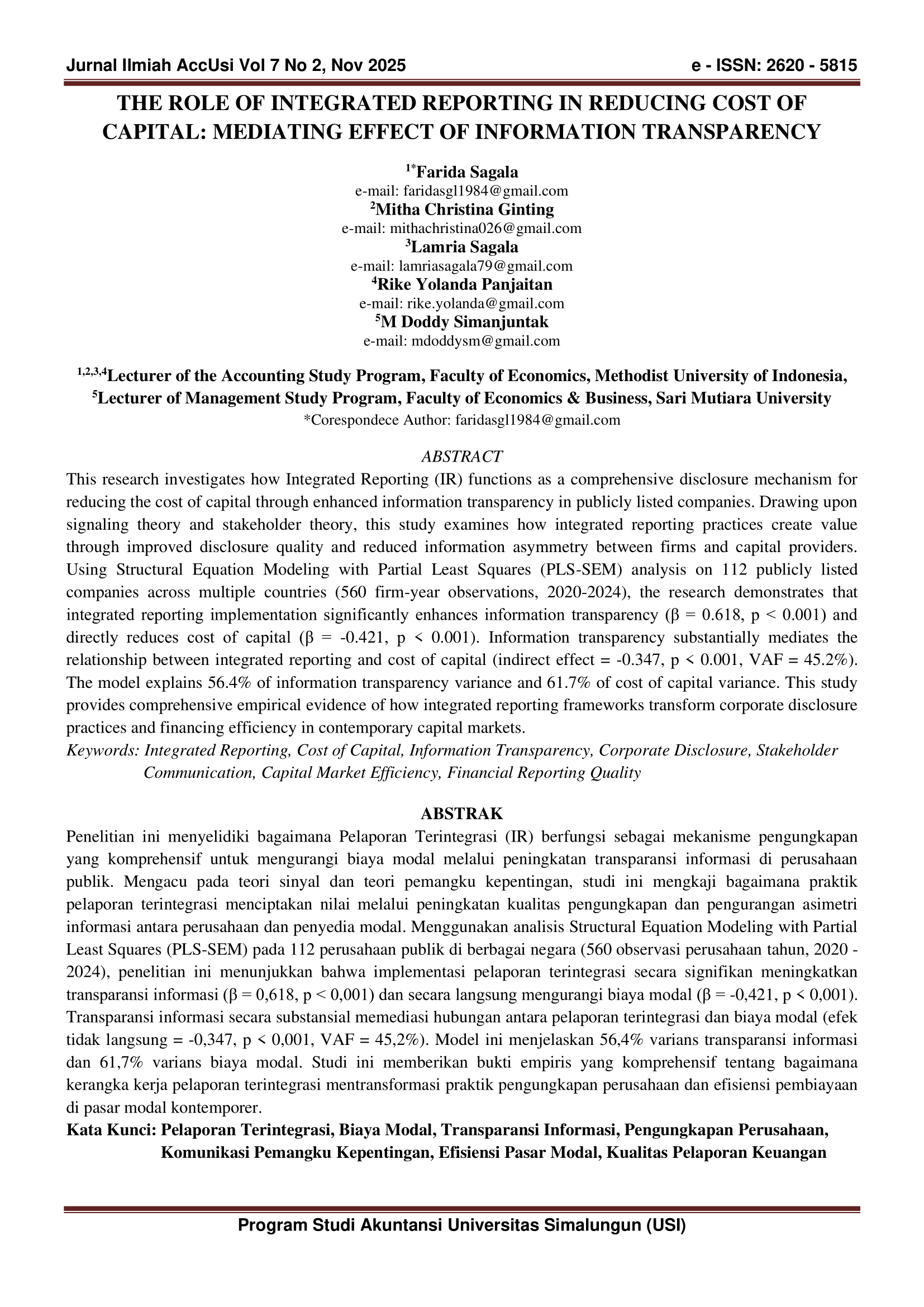

The Role of Integrated Reporting in Reducing Cost of Capital: Mediating Effect of Information Transparency

DOI:

https://doi.org/10.36985/7wwfsc65Keywords:

Integrated Reporting, Cost of Capital, Information Transparency, Corporate Disclosure, Stakeholder Communication, Capital Market Efficiency, Financial Reporting QualityAbstract

This research investigates how Integrated Reporting (IR) functions as a comprehensive disclosure mechanism for reducing the cost of capital through enhanced information transparency in publicly listed companies. Drawing upon signaling theory and stakeholder theory, this study examines how integrated reporting practices create value through improved disclosure quality and reduced information asymmetry between firms and capital providers. Using Structural Equation Modeling with Partial Least Squares (PLS-SEM) analysis on 112 publicly listed companies across multiple countries (560 firm-year observations, 2020-2024), the research demonstrates that integrated reporting implementation significantly enhances information transparency (β = 0.618, p < 0.001) and directly reduces cost of capital (β = -0.421, p < 0.001). Information transparency substantially mediates the relationship between integrated reporting and cost of capital (indirect effect = -0.347, p < 0.001, VAF = 45.2%). The model explains 56.4% of information transparency variance and 61.7% of cost of capital variance. This study provides comprehensive empirical evidence of how integrated reporting frameworks transform corporate disclosure practices and financing efficiency in contemporary capital markets

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Farida Sagala, Mitha Christina Ginting, Lamria Sagala, Rike Yolanda Panjaitan, M Doddy Simanjuntak (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.