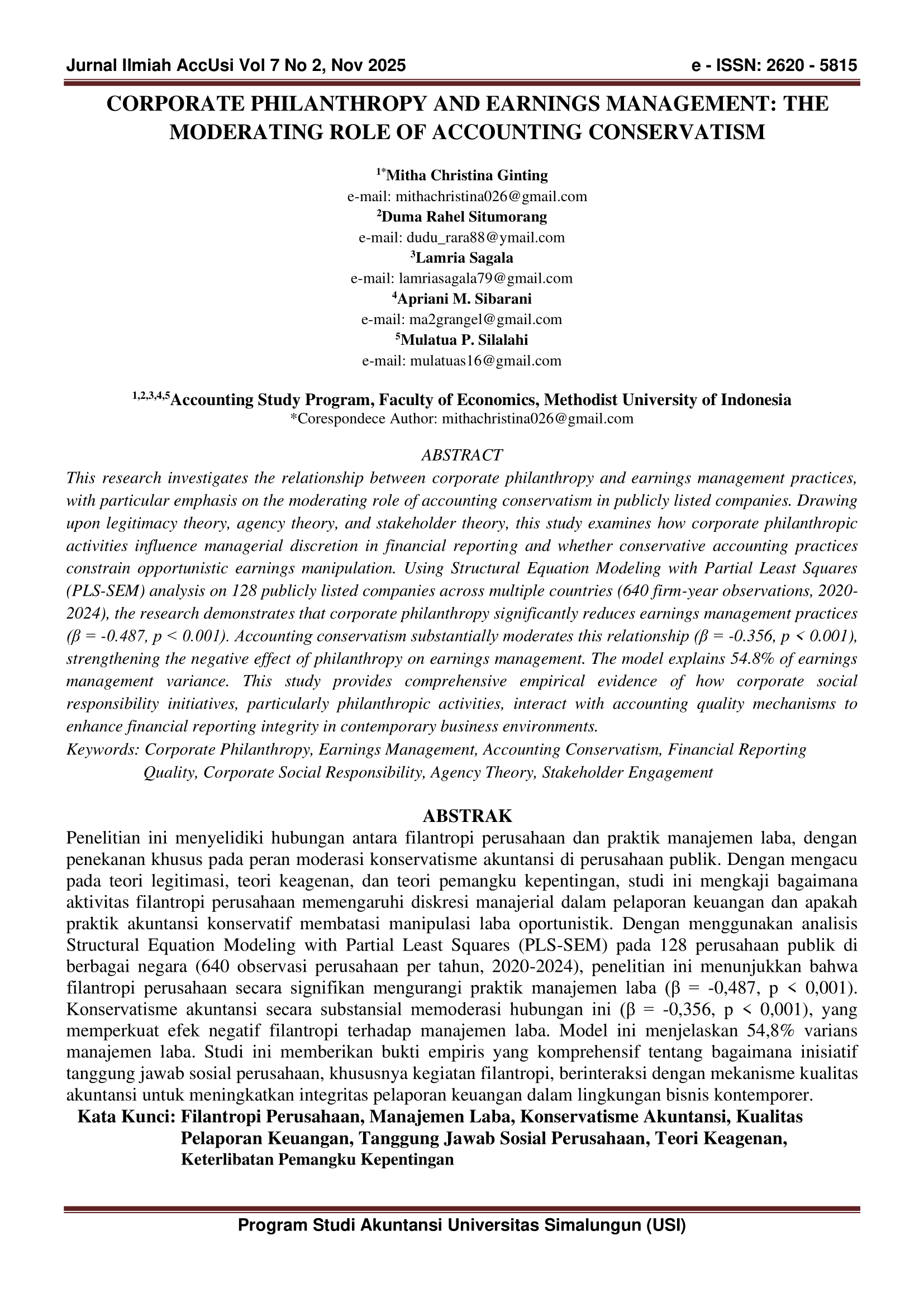

Corporate Philanthropy and Earnings Management: The Moderating Role of Accounting Conservatism

DOI:

https://doi.org/10.36985/7hrk6q26Keywords:

Corporate Philanthropy, Earnings Management, Accounting Conservatism, Financial Reporting Quality, Corporate Social Responsibility, Agency Theory, Stakeholder EngagementAbstract

This research investigates the relationship between corporate philanthropy and earnings management practices, with particular emphasis on the moderating role of accounting conservatism in publicly listed companies. Drawing upon legitimacy theory, agency theory, and stakeholder theory, this study examines how corporate philanthropic activities influence managerial discretion in financial reporting and whether conservative accounting practices constrain opportunistic earnings manipulation. Using Structural Equation Modeling with Partial Least Squares (PLS-SEM) analysis on 128 publicly listed companies across multiple countries (640 firm-year observations, 2020-2024), the research demonstrates that corporate philanthropy significantly reduces earnings management practices (β = -0.487, p < 0.001). Accounting conservatism substantially moderates this relationship (β = -0.356, p < 0.001), strengthening the negative effect of philanthropy on earnings management. The model explains 54.8% of earnings management variance. This study provides comprehensive empirical evidence of how corporate social responsibility initiatives, particularly philanthropic activities, interact with accounting quality mechanisms to enhance financial reporting integrity in contemporary business environments

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Mitha Christina Ginting, Duma Rahel Situmorang, Lamria Sagala, Apriani M Sibarani, Mulatua P Silalahi (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.