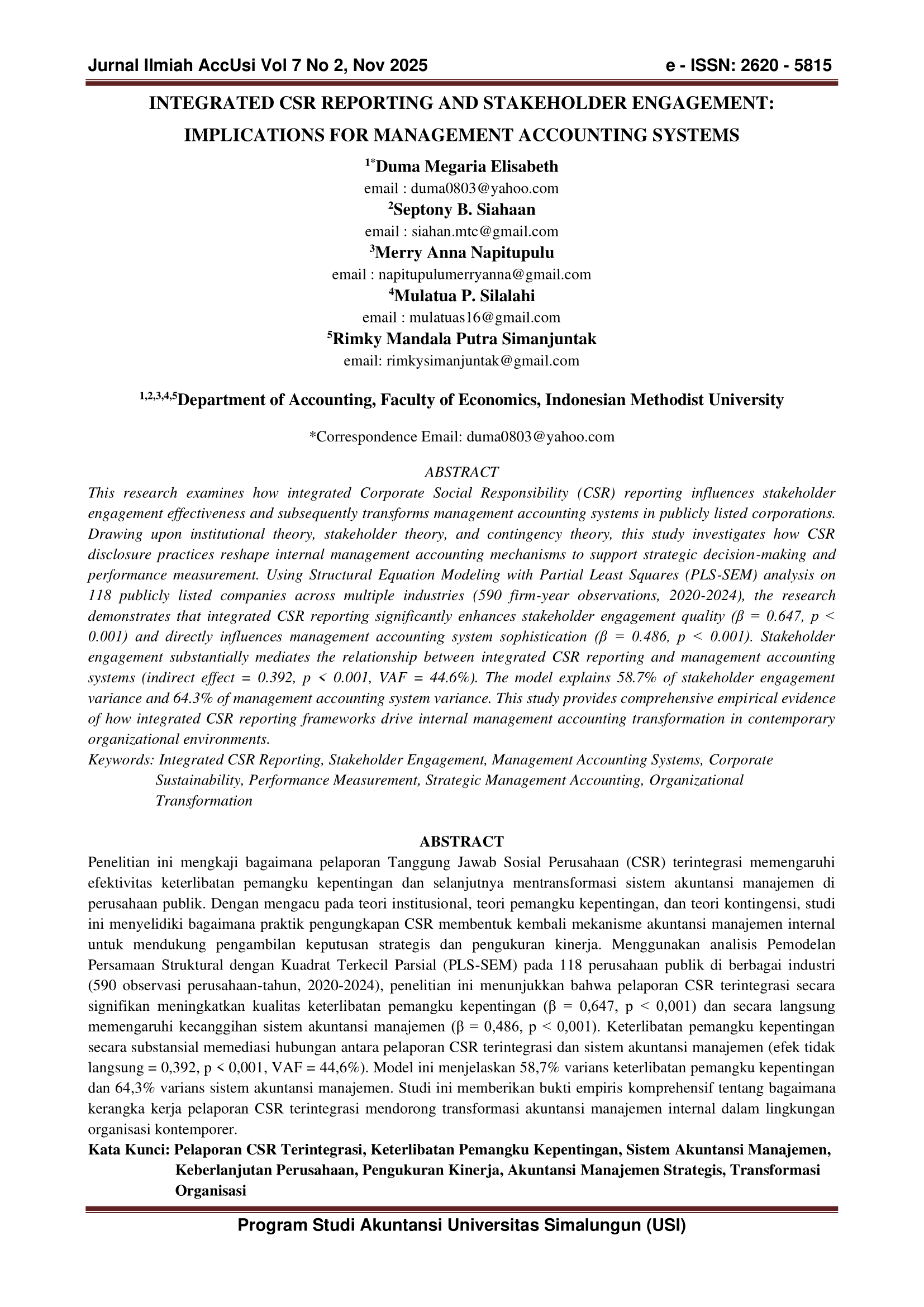

Integrated CSR Reporting and Stakeholder Engagement: Implications for Management Accounting Systems

DOI:

https://doi.org/10.36985/ncvt4p05Keywords:

Integrated CSR Reporting, Stakeholder Engagement, Management Accounting Systems, Corporate Sustainability, Performance Measurement, Strategic Management Accounting, Organizational TransformationAbstract

This research examines how integrated Corporate Social Responsibility (CSR) reporting influences stakeholder engagement effectiveness and subsequently transforms management accounting systems in publicly listed corporations. Drawing upon institutional theory, stakeholder theory, and contingency theory, this study investigates how CSR disclosure practices reshape internal management accounting mechanisms to support strategic decision-making and performance measurement. Using Structural Equation Modeling with Partial Least Squares (PLS-SEM) analysis on 118 publicly listed companies across multiple industries (590 firm-year observations, 2020-2024), the research demonstrates that integrated CSR reporting significantly enhances stakeholder engagement quality (β = 0.647, p < 0.001) and directly influences management accounting system sophistication (β = 0.486, p < 0.001). Stakeholder engagement substantially mediates the relationship between integrated CSR reporting and management accounting systems (indirect effect = 0.392, p < 0.001, VAF = 44.6%). The model explains 58.7% of stakeholder engagement variance and 64.3% of management accounting system variance. This study provides comprehensive empirical evidence of how integrated CSR reporting frameworks drive internal management accounting transformation in contemporary organizational environments

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Duma Megaria Elisabeth, Septony B Siahaan, Merry Anna Napitupulu, Mulatua P Silalahi, Rimky Mandala Putra Simanjuntak (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.