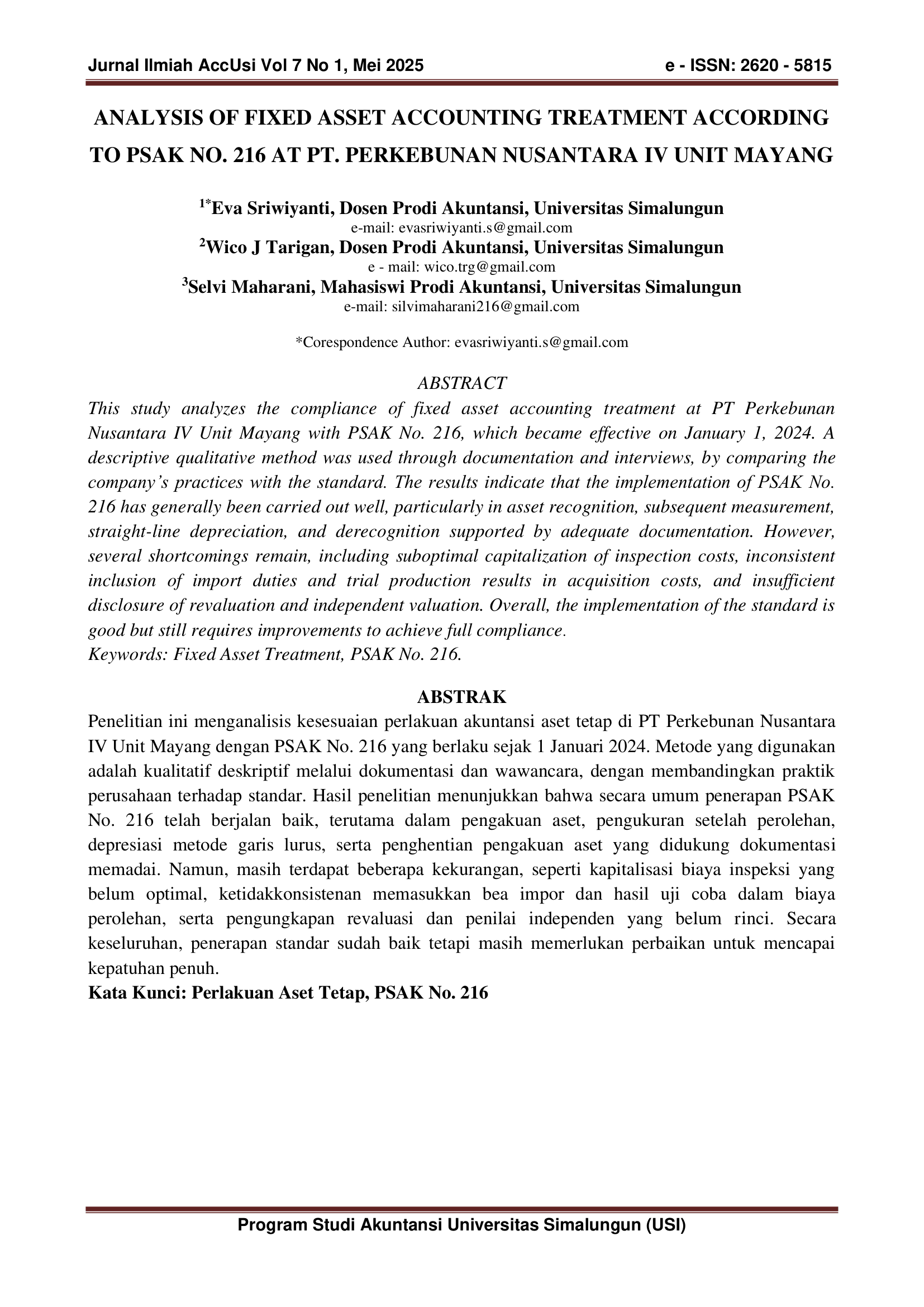

Analysis of Fixed Asset Accounting Treatment According to PSAK NO. 216 at PT. Perkebunan Nusantara IV Unit Mayang

DOI:

https://doi.org/10.36985/g62yax10Keywords:

Fixed Asset Treatment, PSAK No. 216Abstract

This study analyzes the compliance of fixed asset accounting treatment at PT Perkebunan Nusantara IV Unit Mayang with PSAK No. 216, which became effective on January 1, 2024. A descriptive qualitative method was used through documentation and interviews, by comparing the company’s practices with the standard. The results indicate that the implementation of PSAK No. 216 has generally been carried out well, particularly in asset recognition, subsequent measurement, straight-line depreciation, and derecognition supported by adequate documentation. However, several shortcomings remain, including suboptimal capitalization of inspection costs, inconsistent inclusion of import duties and trial production results in acquisition costs, and insufficient disclosure of revaluation and independent valuation. Overall, the implementation of the standard is good but still requires improvements to achieve full compliance

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Eva Sriwiyanti, Wico J Tarigan, Selvi Maharani (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.