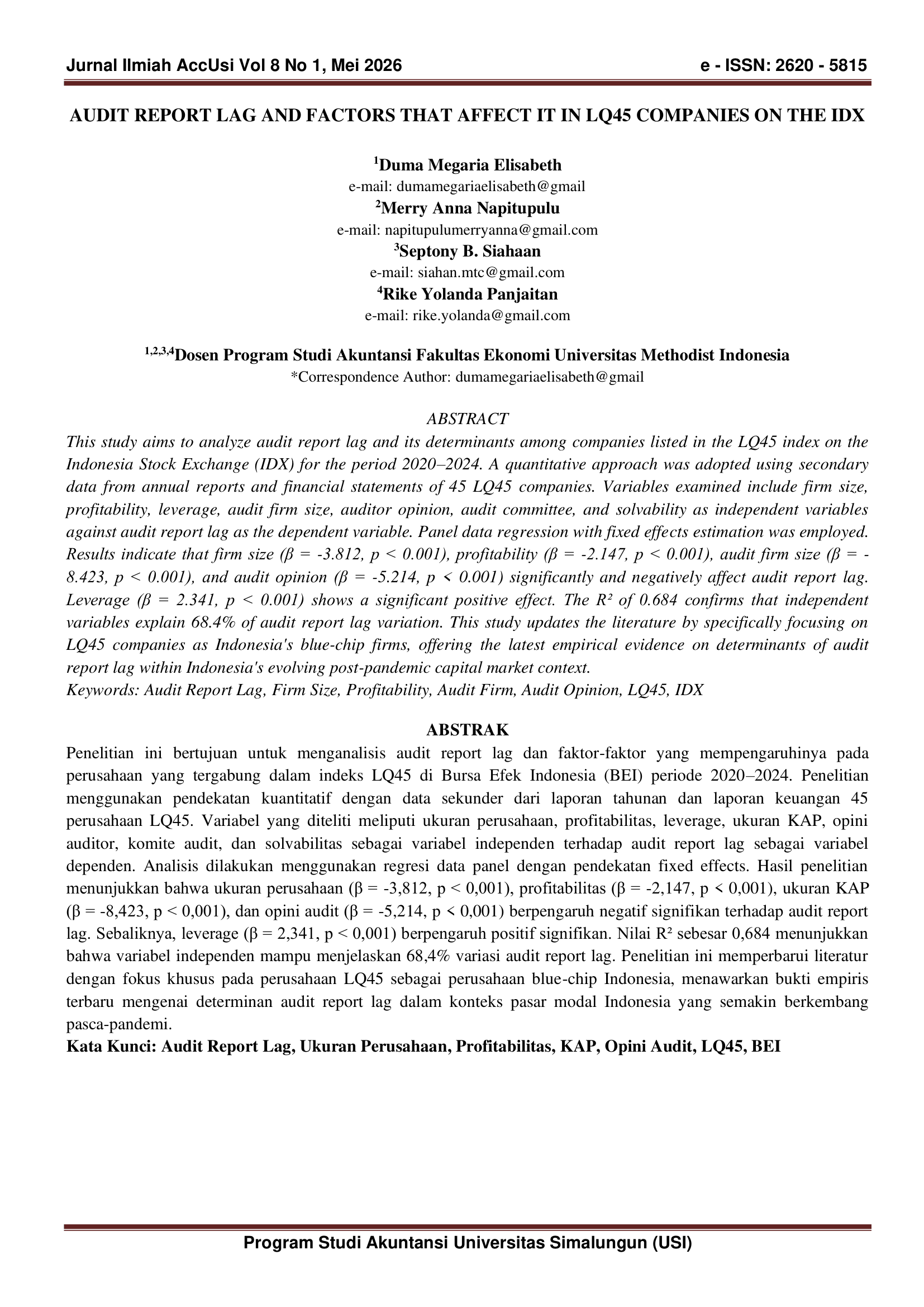

Audit Report Lag and Factors That Affect It in LQ45 Companies On The IDX

DOI:

https://doi.org/10.36985/6tsbb603Keywords:

Audit Report Lag, Firm Size, Profitability, Audit Firm, Audit Opinion, LQ45, IDXAbstract

This study aims to analyze audit report lag and its determinants among companies listed in the LQ45 index on the Indonesia Stock Exchange (IDX) for the period 2020–2024. A quantitative approach was adopted using secondary data from annual reports and financial statements of 45 LQ45 companies. Variables examined include firm size, profitability, leverage, audit firm size, auditor opinion, audit committee, and solvability as independent variables against audit report lag as the dependent variable. Panel data regression with fixed effects estimation was employed. Results indicate that firm size (β = -3.812, p < 0.001), profitability (β = -2.147, p < 0.001), audit firm size (β = -8.423, p < 0.001), and audit opinion (β = -5.214, p < 0.001) significantly and negatively affect audit report lag. Leverage (β = 2.341, p < 0.001) shows a significant positive effect. The R² of 0.684 confirms that independent variables explain 68.4% of audit report lag variation. This study updates the literature by specifically focusing on LQ45 companies as Indonesia's blue-chip firms, offering the latest empirical evidence on determinants of audit report lag within Indonesia's evolving post-pandemic capital market context.

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2026 Duma Megaria Elisabeth, Merry Anna Napitupulu, Septony B Siahaan, Rike Yolanda Panjaitan (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.