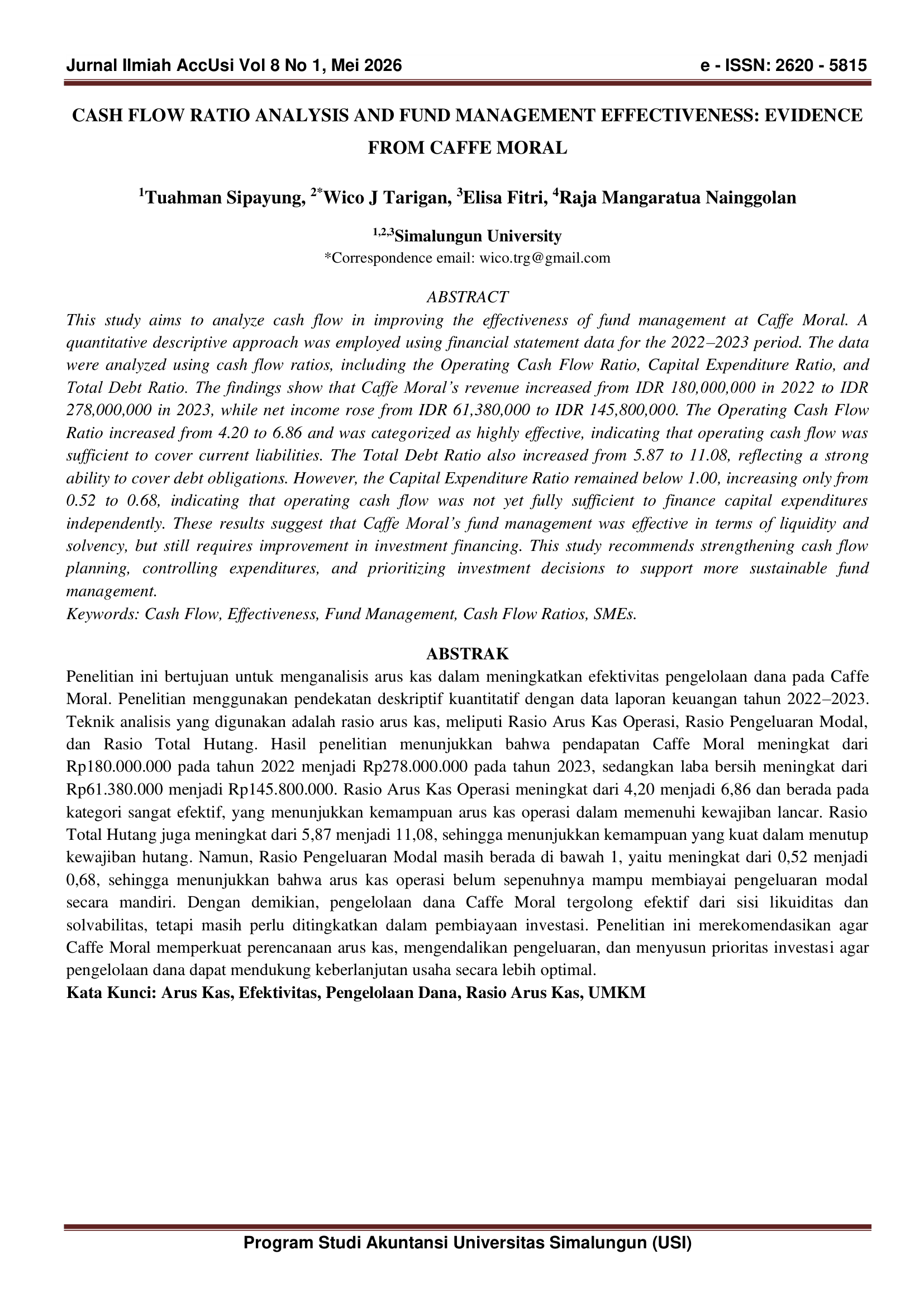

Cash Flow Ratio Analysis and Fund Management Effectiveness: Evidence from Caffe Moral

DOI:

https://doi.org/10.36985/v251vf23Keywords:

Cash Flow, Effectiveness, Fund Management, Cash Flow Ratios, SMEsAbstract

This study aims to analyze cash flow in improving the effectiveness of fund management at Caffe Moral. A quantitative descriptive approach was employed using financial statement data for the 2022–2023 period. The data were analyzed using cash flow ratios, including the Operating Cash Flow Ratio, Capital Expenditure Ratio, and Total Debt Ratio. The findings show that Caffe Moral’s revenue increased from IDR 180,000,000 in 2022 to IDR 278,000,000 in 2023, while net income rose from IDR 61,380,000 to IDR 145,800,000. The Operating Cash Flow Ratio increased from 4.20 to 6.86 and was categorized as highly effective, indicating that operating cash flow was sufficient to cover current liabilities. The Total Debt Ratio also increased from 5.87 to 11.08, reflecting a strong ability to cover debt obligations. However, the Capital Expenditure Ratio remained below 1.00, increasing only from 0.52 to 0.68, indicating that operating cash flow was not yet fully sufficient to finance capital expenditures independently. These results suggest that Caffe Moral’s fund management was effective in terms of liquidity and solvency, but still requires improvement in investment financing. This study recommends strengthening cash flow planning, controlling expenditures, and prioritizing investment decisions to support more sustainable fund management

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2026 Tuahman Sipayung, Wico J Tarigan, Elisa Fitri, Raja Mangaratua Nainggolan, Yesni Riana Damanik (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.