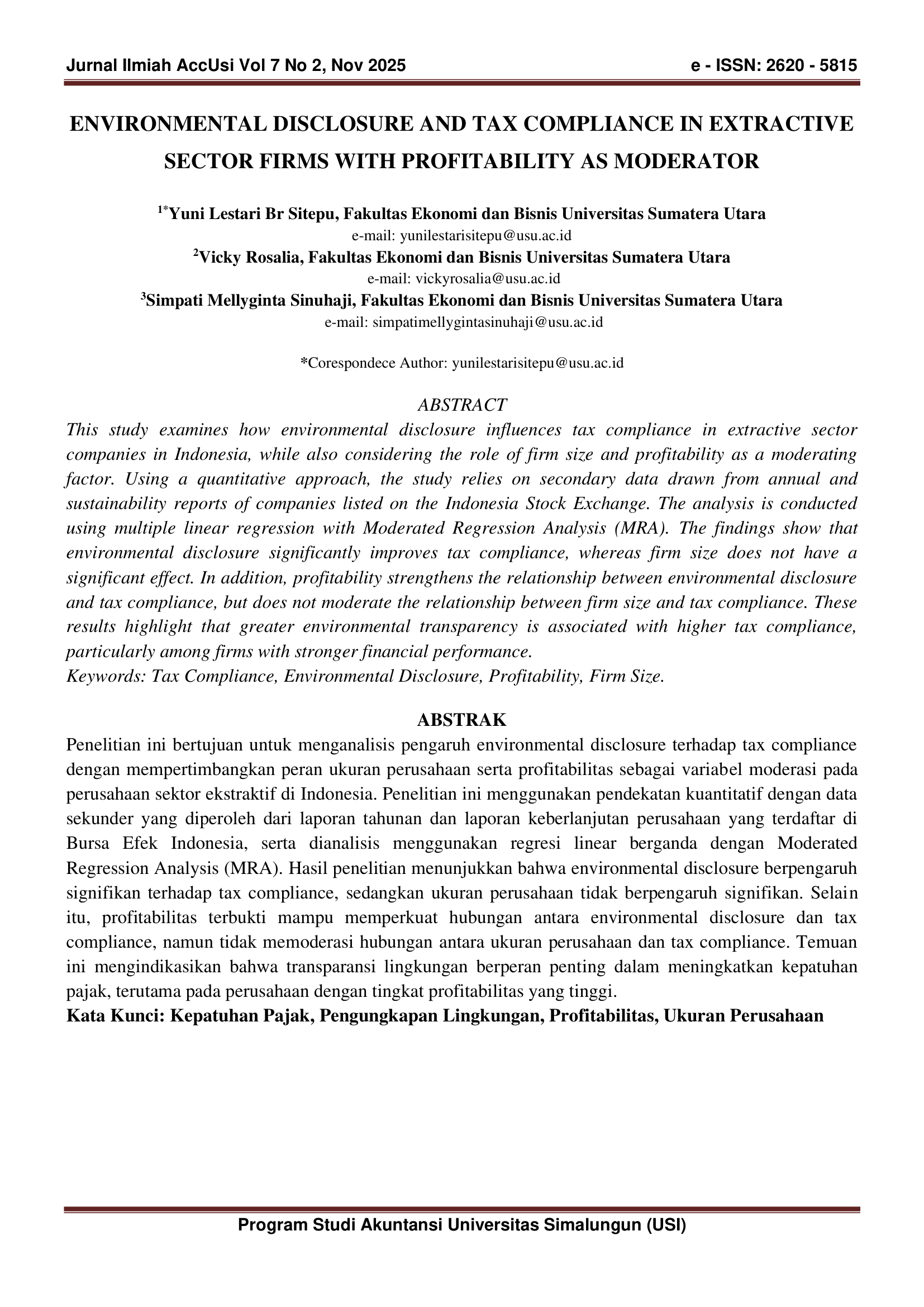

Environmental Disclosure and Tax Compliance in Extractive Sector Firms with Profitability as Moderator

DOI:

https://doi.org/10.36985/92cn0369Keywords:

Tax Compliance, Environmental Disclosure, Profitability, Firm SizeAbstract

This study examines how environmental disclosure influences tax compliance in extractive sector companies in Indonesia, while also considering the role of firm size and profitability as a moderating factor. Using a quantitative approach, the study relies on secondary data drawn from annual and sustainability reports of companies listed on the Indonesia Stock Exchange. The analysis is conducted using multiple linear regression with Moderated Regression Analysis (MRA). The findings show that environmental disclosure significantly improves tax compliance, whereas firm size does not have a significant effect. In addition, profitability strengthens the relationship between environmental disclosure and tax compliance, but does not moderate the relationship between firm size and tax compliance. These results highlight that greater environmental transparency is associated with higher tax compliance, particularly among firms with stronger financial performance

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Yuni Lestari Br Sitepu, Vicky Rosalia, Simpati Mellyginta Sinuhaji (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.