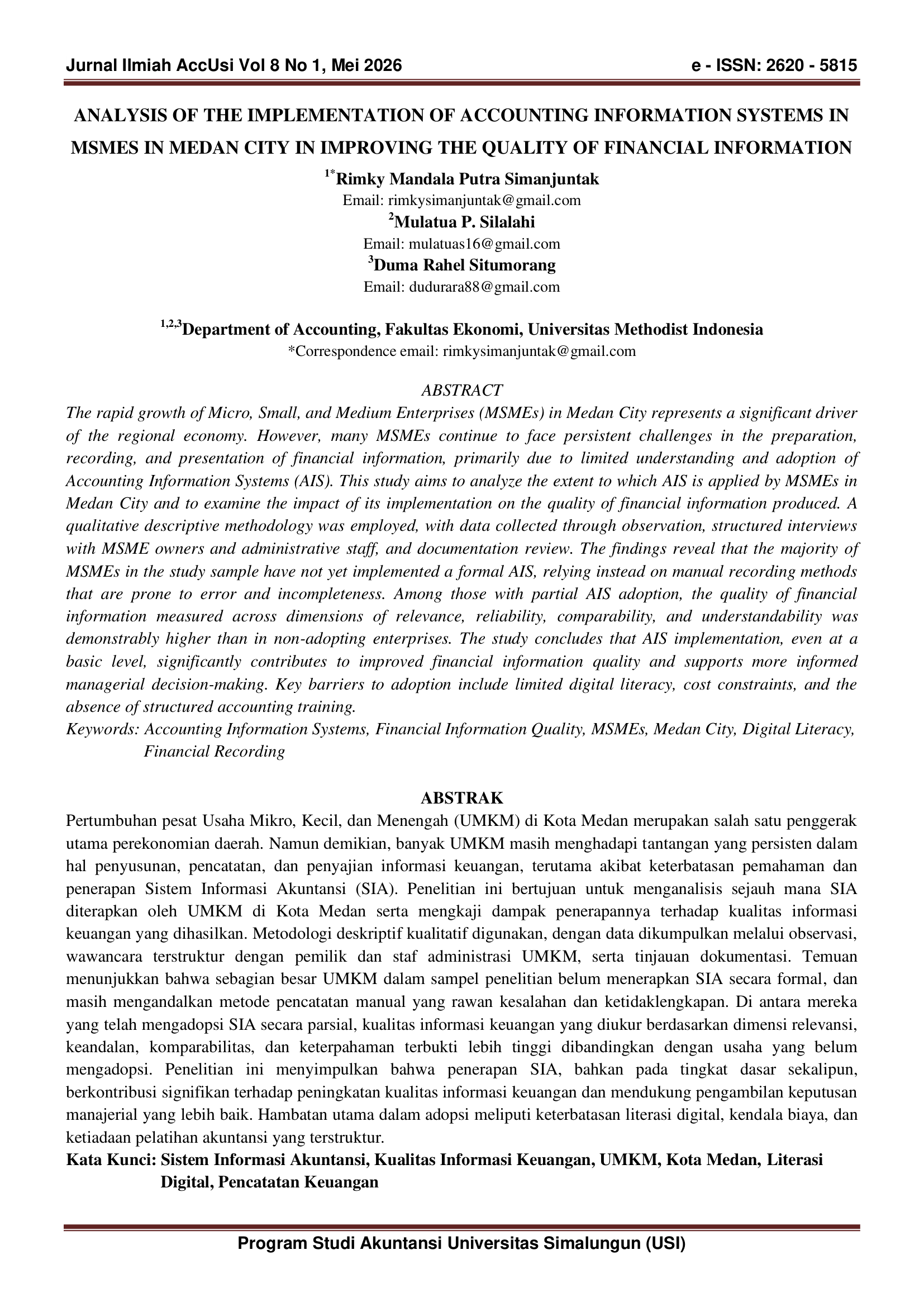

Analysis Of the Implementation of Accounting Information Systems in MSMEs in Medan City in Improving the Quality of Financial Information

DOI:

https://doi.org/10.36985/9y1pvh55Keywords:

Accounting Information Systems, Financial Information Quality, MSMEs, Medan City, Digital Literacy, Financial RecordingAbstract

The rapid growth of Micro, Small, and Medium Enterprises (MSMEs) in Medan City represents a significant driver of the regional economy. However, many MSMEs continue to face persistent challenges in the preparation, recording, and presentation of financial information, primarily due to limited understanding and adoption of Accounting Information Systems (AIS). This study aims to analyze the extent to which AIS is applied by MSMEs in Medan City and to examine the impact of its implementation on the quality of financial information produced. A qualitative descriptive methodology was employed, with data collected through observation, structured interviews with MSME owners and administrative staff, and documentation review. The findings reveal that the majority of MSMEs in the study sample have not yet implemented a formal AIS, relying instead on manual recording methods that are prone to error and incompleteness. Among those with partial AIS adoption, the quality of financial information measured across dimensions of relevance, reliability, comparability, and understandability was demonstrably higher than in non-adopting enterprises. The study concludes that AIS implementation, even at a basic level, significantly contributes to improved financial information quality and supports more informed managerial decision-making. Key barriers to adoption include limited digital literacy, cost constraints, and the absence of structured accounting training

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2026 Rimky Mandala Putra Simanjuntak, Mulatua P Silalahi, Duma Rahel Situmorang (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.