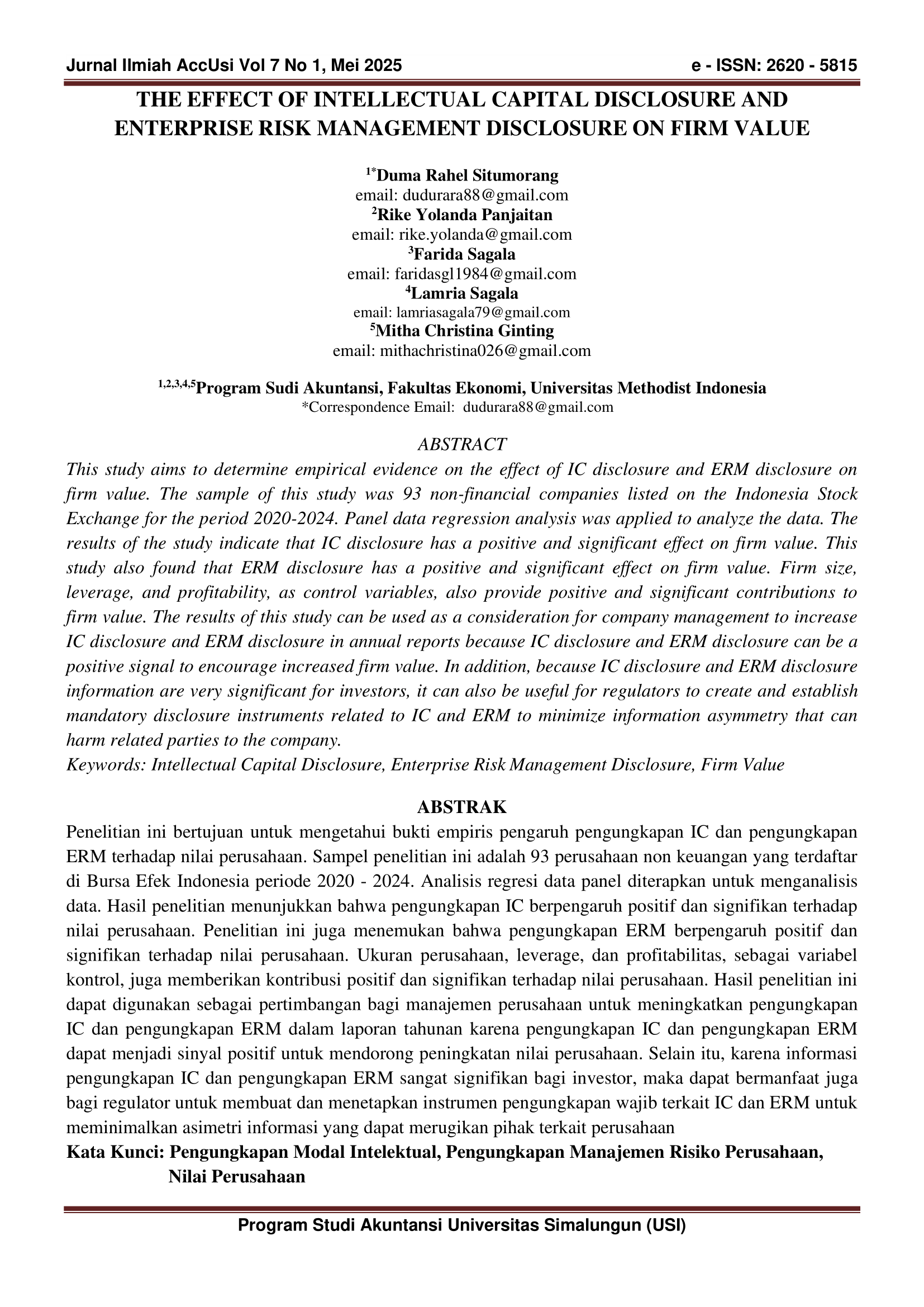

The Effect of Intellectual Capital Disclosure And Enterprise Risk Management Disclosure On Firm Value

DOI:

https://doi.org/10.36985/3ym9h670Keywords:

Intellectual Capital Disclosure, Enterprise Risk Management Disclosure, Firm ValueAbstract

This study aims to determine empirical evidence on the effect of IC disclosure and ERM disclosure on firm value. The sample of this study was 93 non-financial companies listed on the Indonesia Stock Exchange for the period 2020-2024. Panel data regression analysis was applied to analyze the data. The results of the study indicate that IC disclosure has a positive and significant effect on firm value. This study also found that ERM disclosure has a positive and significant effect on firm value. Firm size, leverage, and profitability, as control variables, also provide positive and significant contributions to firm value. The results of this study can be used as a consideration for company management to increase IC disclosure and ERM disclosure in annual reports because IC disclosure and ERM disclosure can be a positive signal to encourage increased firm value. In addition, because IC disclosure and ERM disclosure information are very significant for investors, it can also be useful for regulators to create and establish mandatory disclosure instruments related to IC and ERM to minimize information asymmetry that can harm related parties to the company

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Duma Rahel Situmorang, Rike Yolanda Panjaitan, Farida Sagala, Lamria Sagala, Mitha Christina Ginting (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.